It’s estimated that nearly 40% of Kenyans borrow from digital lenders. That is 18% more than India and 20% more than Pakistan, according to the report, which is alarming and explains the overwhelming number of loan apps in Kenya.

Another report by theafricareport even shows that 62% of borrowers first turn to digital lenders before considering their close friends and family. Kenyans, especially the youth, are becoming entrapped by these mobile lenders and can’t break free.

While most of these lenders used to only lend to borrowers with good credit histories, some no longer care, and you wonder why.

Well, that’s because they have devised devious antics to force the borrowers to pay even if they are already on CRB’s wrong side. It’s business for them, and no business guarantees monstrous profit like lending at high interest.

BEFORE YOU CONTINUE…

My name is Alex Mwangi, founder of centwarrior.com, and I help entrepreneurs, professionals, and individuals protect their income, lifestyle, and wealth, through a solid protection plan.

I have helped hundreds of people protect themselves from illness and their families from imminent poverty when they pass on.

We all know that Life is full of uncertainties, but your family’s future doesn’t have to be one of them.

I will help you get a Life Protection Cover, designed to PROTECT your INCOME and secure the financial future of your loved ones, by providing a lump sum of cash when you pass on.

This Life Protection Cover steps in to effectively replace your income ensuring your family can maintain their current standard of living, covering essential expenses like rent, mortgage, education, and daily needs.

You are also able to protect yourself through Living Benefits that pay out a lump sum in the case you are diagnosed with Accidental Disability or Critical Illnesses such as Cancer, Heart Attack, Coma, Stroke, Open Heart Surgery, and Paralysis/Paraplegia.

Start Your Protection Journey by Filling out this FORM and I will help you get started.

Before You Go..

Here is another FREE gift that will change your life forever (The 7-Step Wealth Master Plan E-Book To Financial Freedom)

How about you? Are you always looking for the next mobile loan app to borrow from?

I’ll expose you to the dangers of such a move and why you should avoid these digital lenders like the plague. I’ll also give you 10 workable ways to avoid this debt cycle trap and attain your financial freedom.

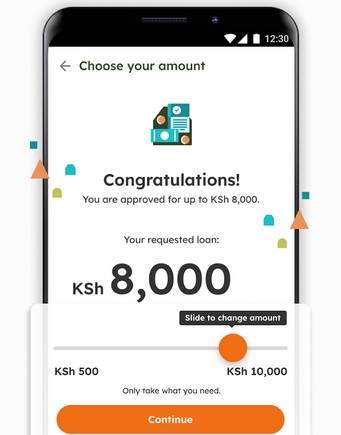

In a rush? Below are Kenya’s 32 most popular loan apps, their loan limits, and their interests.

32 Most Popular Loan Apps in Kenya with Low Interest

| – | Loan App | Loan Limit | Interest | Loan Tenure |

| 1. | Tala | Ksh 2,000 – Ksh 30,000 | 15% of the loan | 14 days |

| 2. | Direct Cash | Ksh 1,500 – Ksh 50,000 | 36% per annum | 91-365 days |

| 3. | Hustler Fund | Ksh 500 – Ksh 50,000 | 8% per annum | 14 days |

| 4. | Meta Loan | Ksh 1,000 – Ksh 80,000 | 4% of the loan | 7-90 days |

| 5. | Branch | Ksh 150 – Ksh 100,000 | 2-18% of the loan | 62 days |

| 6. | Zash | Ksh 500 – Ksh 50,000 | 25% per annum | 91-365 days |

| 7. | Mokash | Ksh 1,000 – Ksh 30,000 | 25% of the loan | 14 days |

| 8. | Bayes | Ksh 1,000 – Ksh 50,000 | 30% per annum | 90-180 days |

| 9. | Opesa | Ksh 1,500 – Ksh 50,000 | 16-29% of the loan | 14 days |

| 10. | Okash | Ksh 500 – Ksh 50,000 | 25-36% of the loan | 21 days |

| 11. | Lion Cash | Ksh 500 – Ksh 70,000 | 16% of the loan | 14 days |

| 12. | Patron | Ksh 200 – Ksh 15,000 | 365-1825% per annum | 91-365 days |

| 13. | Pesa Pap | Ksh 1,000 – Ksh 50,000 | 6.62% of the loan | 30 days |

| 14. | iPesa | Ksh 500 — Ksh 50,000 | 18% of the loan | 14 days |

| 15. | Asap Kash | Ksh 1,000 – Ksh 12,000 | 18% per annum | 91-365 days |

| 16. | Apesa | Ksh 500 – Ksh 8,000 | 18% per annum | 91-365 days |

| 17. | KashWay | Ksh 500 – Ksh 60,000 | 25-36% of the loan | 14 days |

| 18. | Fadhili | From Ksh 500 | 24% per annum | 21 days |

| 19. | Credit Moja | Ksh 2,500 – Ksh 25,000 | Up to 50% per annum | 91-365 days |

| 20. | InstaPesa | Ksh 3,000 – Ksh 80,000 | 8-20% of the loan | 91-365 days |

| 21. | KCB MPESA | From Ksh 1,000 | 8.64% of the loan | 30 days |

| 22. | Fuliza MPESA | Ksh 1 – Ksh 70,000 | Ksh 2 – Ksh 25 per day | 30 days |

| 23. | Timiza | Ksh 500 – Ksh 100,000 | 1.083% of the loan | 30 days |

| 24. | NCBA Loop | Up to Ksh 3 million | 2% facility fee + 10% excise duty | 6-36 months |

| 25. | Eazzy Loan | From Ksh 1,000 | 13% per annum | 1-12 months |

| 26. | VOOMA Loan | Up to Ksh 300,000 | 7.13%% of the loan | 30 days |

| 27. | HF Whizz | Ksh 1,000 – Ksh 50,000 | 10% of the loan | 30 days |

| 28. | MCOOP Cash | Ksh 1,000 – Ksh 500,000 | 8% per month | 1-3 months |

| 29. | Pesa Pata | Ksh 500 – Ksh 20,000 | 10-30% of the loan | 30 days |

| 30. | Zenka | Ksh 500 – Ksh 30,000 | 9-30% of the loan | 61 days |

| 31. | FlashPesa | Ksh 2,000 – Ksh 50,000 | 15-25% of the loan | 31 days |

| 32. | Berry App | Ksh 500 – Ksh 50,000 | 8-15% of the loan | 30-120 days |

32 Most Popular Loan Apps in Kenya Reviewed

Here are 32 most popular loan apps in kenya right now:

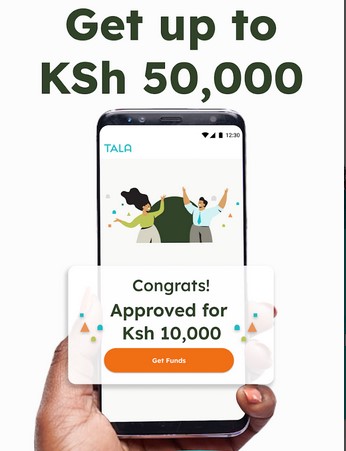

1. Tala Loan App

Tala is a popular mobile loan app by Indian-born American businesswoman Shivani Siroya, who founded the lending app in 2011. So, Tala is, without a doubt, one of the oldest mobile apps in the country.

With Tala, you can borrow Ksh 2,000 – Ksh 30,000, depending on your creditworthiness. Tala loans mostly come with a 14-day repayment period and attract a 15% interest.

After failing to beat the deadline, Tala levies an 8% flat rate penalty. You need a smartphone, national ID, and good CRB standing to qualify for a Tala loan.

2. Direct Cash

Direct Cash is a loan app by Direct Cash Kenya that offers loans from Ksh 1,500 to Ksh 50,000. According to the lender, these loans are payable within 91 – 365 days and attract an annual interest rate of 36%.

Direct Cash has been operational since 2020, making it one of the newest entrants into the Kenya digital lending space. In addition to the interest rate, Direct Cash charges a 1 – 9% origination fee.

3. Hustler Fund

The Hustler Fund is a government-supported digital lender that allows individuals to borrow Ksh 500 – Ksh 50,000 and registered groups or Chamas up to Ksh 1 million.

For individual loans, you’ve up to 14 days to repay the loan at an annual interest of 8%. Failure to do that will result in a rollover penalty of 9.5%.

The Hustler Fund is the least expensive to pay and easiest to qualify for, even with CRB blacklisting. Its 14-day repayment period, however, is not the most flexible, you must agree.

4. Meta Loan App

Meta Loan is a loan product by Zillions Credit Company, the same company that owns the Zash loan app. The lender allows you to borrow Ksh 1,000 – Ksh 80,000 depending on eligibility, and the loans attract an interest rate of 4% of the loan amount.

According to Meta Loan, you have 7 – 90 days to repay the loan and don’t need a credit record to apply for one. However, you must be 18 – 60 years old, have a Kenyan ID, and have an income source.

5. Branch Loan

Branch is a product of Branch Microfinance, a deposit-taking Central Bank-registered microfinance bank in Kenya. The lender has been running since 2006 and offers mobile loans ranging from Ksh 150 to about Ksh 100,000, depending on eligibility.

Branch loans have a maximum repayment period of 62 days, attracting an interest rate of 2 – 28% of the loan amount. So far, there are no late fees or withdrawal charges. You must be in good standing with CRB and have an ID and active M-PESA account to qualify for a Branch loan.

6. Zash Loan App

Zash is a digital lending service by Zillions Credit Ltd that was only released recently (June 2023). This mobile lender allows you to borrow Ksh 500 – Ksh 50,000, and you’ve 7 – 91 days to pay it back in full.

Zash mobile loans attract an interest rate of 25% of the loan amount (which they also call the processing fee)—Failure to beat Zash’s short-term deadline results in a 2.5% daily penalty.

You need good CRB standing, an Android phone, a national ID, and an M-PESA registered line to qualify for a Zash loan.

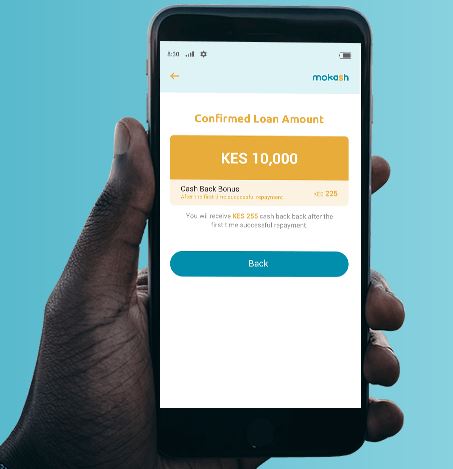

7. Mokash Loan App

Mokash is a loan offered by MOCASH Kenya that lets you borrow Ksh 1,000 – Ksh 30,000. Currently, Mokash charges an interest rate of 26% of the loan amount, and you have up to 14 days to repay your loan.

Failure to beat the 2-week deadline attracts a 2% daily penalty until you pay everything in full. Mokash expects you to have a good CRB score, smartphone, national ID (at least 20 years), and an active M-PESA account to apply for a loan.

8. Bayes

Bayes is a loan product by Pi Capital, offering Ksh 1,000 – Ksh 500,000, depending on eligibility. The Lender charges you a 30% interest rate (of the principal amount), and you’ve 14 – 30 days to repay the loan.

After that, Bayes can offer you a 3-day grace period, after which the lender may take action. The action may involve blacklisting you with CRB.

9. Opesa

Opesa is a digital loan product by TenSport Kenya Ltd that allows you to borrow Ksh 1,500 – Ksh 50,000 and pay it within 14 days. All Opesa loans attract an interest of 16 – 29 % of the loan amount.

While there’s no processing or withdrawal fee, as far as we can tell, the lender charges a 2.4% daily late fee for failing to beat the deadline. Good CRB standing, an ID, a smartphone, and an active M-PESA account are vital eligibility requirements.

10. Okash

Okash is a mobile credit product by Opera Group through which TenSport Kenya Ltd runs it. Qualified borrowers can borrow Ksh 500 – Ksh 50,000 depending on eligibility, and each loan attracts an annual interest of 36%.

According to Okash, their loans have a 91 – 365-day repayment period. Customer reviews, however, show that the interest is 25 – 36% of the loan amount, and loans are payable within 21 days. Failure to beat the 3-week deadline attracts a 2% daily late fee.

11. Lion Cash

Lion Cash is a digital lending platform by Grola Tech Limited. This digital lender is also present in Nigeria. Depending on eligibility, you can get a loan from Ksh 500 to Ksh 70,000 from Lion Cash, and the loans attract an interest of 16%.

Lion Cash loans are payable within 14 days. Failure to beat the 2-week deadline attracts a 2% daily late fee.

You need good CRB standing, a smartphone, a national ID, and an active M-PESA account to apply.

12. Patron

Patron is a new mobile lender that offers its customers smaller instant loans of Ksh 200 – Ksh 15,000. So, you don’t get a lot from them.

In terms of interest, Patron charges 365 – 1825% per annum, which you must agree is a lot, even if you have up to 91 – 365 days to pay back.

Though Patron doesn’t do CRB checks when offering its loan, you must be employed to qualify. In that case, you must provide a pay slip or any other recognized proof of employment.

13. Pesa Pap

Pesa app is a digital wallet, online banking app, and digital lender by Family Bank, which lends to you Ksh 1,000 – Ksh 50,000 via your mobile phone.

These mobile loans attract an interest rate of 6.62% of the loan amount, and you have a 30-day repayment period. The 6.62% interest is broken down as follows:

- 5% loan processing fee

- 1.12% monthly interest

- 0.5% insurance fee

14. iPesa Loan App

iPesa is one of the most downloaded mobile loan apps on Google Play. This loan product by iPesa Limited allows you to borrow Ksh 500 – Ksh 50,000 at an interest rate of 18% of the loan amount.

The loan terms start from 14 days, and failure to beat the short-term deadline attracts a 2% daily penalty. You need good CRB standing, a smartphone, M-PESA registered line, and a valid national ID to qualify for an iPesa mobile loan.

15. Asap Kash

Asap Kash promises mobile loans starting from Ksh 1,000 to about Ksh 12,000. So, they also don’t offer a vast loan limit. Asap Kash charges an annual interest rate of 18%, and you have up to 91 – 365 days to repay the loan.

16. Apesa

Apesa offers mobile loans attesting from Ksh 500 to about Ksh 8,000, which is not a lot but just enough. All Apesa loans attract an interest rate of 18% per annum, and like Asap Kash, you’ve up to 91 – 365 days to pay back the loan.

17. Kashway

Kashway is a mobile credit product by Wakanda Credit Limited, released on 9th January 2020. This digital lender allows you to borrow Ksh 500 – Ksh 60,000 depending on creditworthiness, and the loans attract an interest of 25 – 36% of the loan amount.

Kashway expects you to repay its loan within 14 days, after which the lender imposes a 2% daily penalty for late payments. You need good CRB standing, an Android phone, a National ID, and an M-PESA registered line to qualify for a Kashway loan.

18. Fadhili

Fadhili is another popular mobile lender in Kenya that allows you to borrow anything from Ksh 500, depending on eligibility. This lender imposes a 24% annual interest and offers you 21 days to repay the loan.

In addition to the interest, Fadhili charges an account management fee of Ksh 400 annually.

They argue that the account maintenance fee is to detract non-committed borrowers, but if you ask me, that’s another way to rob you of your hard-earned money.

19. Credit Moja

Credit Moja is a new entrant into the Kenya digital lending space, lending Ksh 2,500 – Ksh 25,000 to eligible applicants.

The lender charges an annual interest of up to 50% while offering you up to 91 – 365 days (according to the lender). You must be 20 – 55 years old and a Kenyan resident to apply for a Credit Moja loan.

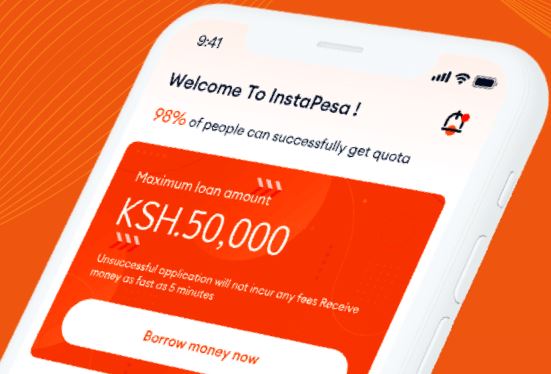

20. Insta Pesa Loan App

Insta Pesa is another digital lender that lets you borrow Ksh 3,000 – Ksh 80,000, depending on eligibility. So, their loan limits are pretty good, and so is the repayment period (91 – 365 days).

The problem, however, is the interest rate of about 8 – 20% of the loan amount. Some customers also claim the loan term is way shorter than the 91 – 365 days that the lender claims.

21. KCB M-PESA

KCB M-PESA is a partnership product between Kenya Commercial Bank (KCB) and mobile money giant M-PESA. These loans start from Ksh 1,000, depending on one’s eligibility, and attract an interest of 8.64% of the loan amount.

KCB M-PESA expects you to pay back your loan within 30 days, failure to which attracts an equal rollover (8.64%) late fee. However, unlike most loan apps, there are no processing fees, insurance fees, or withdrawal charges. You need an excellent CRB standing, ID, and an active M-PESA account (at least six months) to qualify.

22. Fuliza M-PESA

Fuliza is not really a mobile loan but an overdraft service you can access via the M-PESA app or STK route, which enables you to complete a purchase when you lack sufficient funds in your M-PESA account.

Depending on eligibility, you can Fuliza anything from Ksh 1 to Ksh 70,000, and you have up to 30 days to pay it in full. Fuliza loans attract a daily fee of Ksh 2 – Ksh 25, depending on the loan amount.

23. Timiza Loan App

Timiza is a product by Absa Bank Kenya that offers loans from Ksh 500 to Ksh 100,000. Unlike most commercial bank-backed loan products, you don’t have to have an active Timiza bank account to qualify for a Timiza loan.

You must be in good standing with the CRB, have an active M-PESA account (at least six months), and possess an ID.

Overall, Timiza loans attract an interest of 1.083 of the loan amount and are payable within 30 days. However, there is a 5% processing fee, a 20% excise duty on the processing fees, and a 5% rollover fee.

24. NCBA Loop

The NCBA Loop is a loan and mobile banking product by NCBA Bank Kenya that offers loans of up to Ksh 3 million to qualified NCBA customers.

These loans come with a 6 – 36-month repayment period, typically attracting a 2% facility or processing fee and a 10% excise duty. Interest-wise, NCBA loans have a 14.1% annual interest rate.

As far as we know, there are no late fees but withdrawal charges (up to Ksh 42) and a 0.7% insurance fee. You need an active Loop account (at least three months) and good CRB standing to apply for a Loop loan.

25. Eazzy Loan

The Eazzy loan is a mobile loan product by Equity Bank Group that offers loans starting from Ksh 1,000 to eligible applicants. Eazzy loans are usually payable within 1 – 12 months, depending on the loan size, and attract an annual interest of 13%.

Additionally, there’s a 5% processing fee and an equal (5%) late fee for failing to beat the payment deadline. Other charges associated with the Eazzy loans include a 1% insurance fee and a 10% excise duty.

You’ll need an active account of at least six months and good CRB standing to qualify for an Eazzy loan.

26. Vooma Loan App

Vooma is a digital wallet and mobile credit product by KCB Bank. Regarding the loan part, Vooma allows you to borrow Ksh 1,000 – Ksh 300,000 depending on creditworthiness, and you’ve up to 30 days to repay it.

Vooma loans usually attract an interest rate of 7.13% of the loan amount and an equal rollover for late payments. You need an active KCB account (at least six months), make at least four bank deposits within the last six months, and have an ID to qualify for a Vooma loan.

27. HF Whizz

The HF Whizz is a banking app by HFC Group Kenya that allows you to deposit cash, make transfers, and settle bill payments conveniently. But in addition to that, you can borrow Ksh 1,000 – Ksh 50,000 from the app.

HF Whizz loans usually attract an interest of 10% of the loan amount, and you’ve up to 30 days to repay the mobile loan fully.

28. MCOOP Cash

MCOOP Cash is a digital loan product by the Cooperative Bank of Kenya. This mobile loan app lets you borrow Ksh 1,000 – Ksh 500,000, depending on what you qualify for, and generally attracts an interest of 8% per month.

The loans are payable within 1 – 3 months. You need a national ID/passport, a KRA pin, and an active salary account to apply. Overall, you can access your COOP Bank details and mobile bank via MCOOP cash, making things more convenient.

29. Pesa Pata

Pesa Pata is a digital lending platform founded by Joyce Wangui and Samson Wachira that offers mobile loans of about Ksh 500 – Ksh 20,000 and charges an interest of 10 – 30% of the loan, depending on loan size. Overall, Pesa Pata offers you a 30-day repayment period.

30. Zenka Loan App

Zenka is an unsecured mobile loan by Zenka Digital, a licensed credit-only lender. The lender offers loans attesting from Ksh 500 to Ksh 30,000 and attracting an interest of 9 – 30% of the loan amount.

Zenka loans typically have a maximum repayment term of 61 days. Zenka imposes a processing fee of Ksh 45 – Ksh 5,800, depending on the amount, and a 1% daily late fee for failing to beat the deadline.

To qualify, you must be in good CRB standing and have an ID, smartphone, and active M-PESA account.

31. Flash Pesa

Flash Pesa is a mobile loan app by Ambush Capital Limited, a licensed credit-only lender. This lender offers loans of between Ksh 2,000 and Ksh 50,000 to qualified customers, and the loans are payable within 31 days.

Each Flash Pesa loan attracts an interest of 15 – 25% of the loan amount and a processing fee of Ksh 150 – Ksh 600. You need an Android smartphone to download the loan app from Google Play.

Flash Pesa expects you to have good CRB standing, a national ID, and an active M-PESA account to apply for the loan.

32. Berry Loan App

The Berry loan app is a mobile lending service by FinBerry Capital that offers loans of Ksh 500 – Ksh 50,000. This loan app has been in operation since 2018 and charges you an interest rate of 8 – 15% of the loan amount.

Berry loan app offers you up to 30 – 120 days to pay back the loan in full, resulting in a 10% penalty on the loan amount. Unlike most digital lenders, Berry offers you a 7-day extension. They, however, have a monthly facilitation fee of 9 – 25%, which is pretty high.

Leading Loan Apps in Kenya Without Registration Fee and CRB Check

Loan Apps in Kenya Without Registration Fee

While some mobile lenders require you to pay a sign-up fee, others don’t have such charges. They aim to attract borrowers who are conscious of spending money before they can have it.

Some of the leading loan apps in Kenya without registration fees are:

- Tala

- Direct Cash

- Hustler Fund

- Meta Loan

- Branch Loan

- Zash Loan

- Utunzi Loan

- Bayes

- Opesa

- Okash

Check out the loan limits, interest, and loan tenure of the above loan apps in the table shared earlier.

Loan Apps in Kenya Without CRB Check

So many online apps nowadays offer credits without looking at the lender’s credit history. That makes it easy for borrowers on the CRB’s watch list to procure a loan.

Some of the leading loan apps without CRB checks in Kenya are:

- Lion Cash

- Patron

- Pesa Pap

- iPesa

- Asap Kash

- Apesa

- KashWay

- Fadhili

- Credit Moja

- InstaPesa

- Okolea

Note that these loans have been banned from accessing CRB services. You can also refer to the table shared earlier to get their loan limits, interests, and tenures.

Loan Apps in Kenya with USSD

Some mobile loan apps also have the USSD option to cater to those without smartphones or who don’t like installing loan apps on their phones. These mobile emergency loan lenders include:

- KCB MPESA (*844#)

- Fuliza MPESA (*234#)

- Timiza (*848#)

- NCBA Loop (*654#)

- Eazzy Loan (*247#)

- VOOMA Loan (*844#)

- HF Whizz (*618#)

- MCOOP Cash (*667#)

- Pesa Pata (*269#)

- Zenka loan (*841#)

Also, refer to the above table for these lenders’ loan limits, interest, and tenure.

Dangers of Borrowing Via Loan Apps in Kenya

It’s irrefutable that mobile loan apps can come to the rescue when in a financial fix. Yes, you can borrow to pay a bill or make an unplanned but probably essential purchase. They are fast and offer the convenience of having money in your MPESA wallet.

The question is, are they worth it? Should you borrow from these digital lenders? I firmly believe you shouldn’t, and it’s all because of these dangers:

1. Loan Apps Are Expensive to Pay

The Kenyan digital lending space is flocked with many apps because lenders are in for a huge catch. Their goal is to make money out of financially desperate Kenyans, and they lend out with outrageous interest and fees.

Essentially, here are the charges that make mobile loans expensive.

- Monstrous interest – Imagine paying 16 – 25% interest per month or more if you fail to pay on time. Some lenders even charge as high as 365 – 1825% APR as it’s the case of the Patron Loan App, which is just a monstrous fee.

- Hidden charges – The monstrous interest is not the only concern. There are others, such as processing fees, origination fees, excise duty, and registration fees.

- Hefty penalties – Another crafty way these lenders make money is through late payment penalties. They quickly slap you with a higher interest once you fail to pay the loan on time.

2. Privacy Risks

These lenders usually ask for access permission to your phone’s contact list, SMS, and chats, among other private information. But do you ever stop to ask about the implication of that?

Well, it includes the following:

- Harassment – Imagine someone on your contact list receiving a call from the lender asking them to ask you to pay or pay themselves because they were listed as guarantors. That’s wholesome harassment, often when one fails to pay a loan app.

- Extortion – Some lenders lack decency. They resort to using the customers’ personal information to exhort them. And since they are rarely regulated, they can get away with such expenses.

- Possible identity theft – Do you know who is taking your personal information? They could be careless with the information, and someone with bad intentions could use it for who knows what.

3. Short Repayment

I know I’ve indicated in the above table that loan most tenures stretch between 91 – 365 days. However, if you ask most borrowers, these lenders rarely give you more than 30 days to pay back. So, the extended repayment is only for show-off, but expect to pay the loan back in 14 – 30 days.

4. Most Loan Apps Are Fraudulent

Starting January 2023, Google plans to remove some mobile money lenders from Google play for violating CBK rules. The notice came last year, according to an NTV Kenya report.

The move by Google is to try and do away with fraudulent apps robbing Kenyans in the name of offering emergency loans.

Here’s how you can identify a fraudulent loan app or lender:

- The app is no longer on Google Play – You are likely to find it on the company website or through a link

- Unsecured website – If the website URL lacks the padlock symbol or has the HTTP prefix instead of HTTPS, such a website is not secure and likely indicates the lender is fraudulent

- So many negative reviews – If many customers complain about the lender, that’s a red flag.

- No contact information – It’s also a red flag if the lender has no physical address or other contact information.

5. Loan Apps Are a Debt Trap

Last but not least, these loan apps are a debt trap. The lender raises your loan limit not to help you but to improve their chances of making more money out of you.

They recognize that the more they give you, the more you pay back. And since you always want to get a higher limit and possibly improve your credit score, you’ll always try to pay on time.

The danger of that is that you won’t stop borrowing. You don’t realize that you are in a debt trap that sometimes forces you to borrow from one digital lender to pay another.

How to Avoid Falling Victim of the Loan App Trap in Kenya

Now that we’ve addressed the dangers of mobile loan apps, you probably are asking, then what? How do I attend to my financial emergencies?

Well, it takes financial discipline and good planning, and this is what I recommend:

1. Set Up an Emergency Fund

You must agree that financial emergencies like illness, delayed pay, job losses, injuries, and car breakdowns drive most Kenyans to digital lenders.

That, however, shouldn’t be the case if you have an emergency fund (tantamount to your household’s six months’ living expenses). So, consider setting up an emergency fund if you don’t have it.

2. Create A Budget and Stick to It

I like referring to Dave Ramsey’s famous definition of a budget, where he says, “a budget is telling your money where to go and not having to ask where it went.”

Most people who borrow from these loan apps have jobs or businesses, meaning they have a regular income. They, however, resort to borrowing because they can’t budget for what they have.

So, a budget is necessary to avoid any debt trap.

3. Pay Yourself First

According to serial entrepreneur John Rampton, “A cardinal rule in budgeting and saving is to pay yourself first.”

Generally, the personal finance principle of paying yourself first allows you to save up when you receive your income before spending it. So, the bills come after first saving.

That means you’ll have money in your emergency fund to take care of the rainy day.

4. Have A Financial Plan

You must have a financial plan if you intend to stay away from borrowing. The plan shouldn’t just feature your budget but also your savings plan, investment plan, and debt repayment plan. Don’t forget, however, about investment.

5. Prioritize Needs

You’ve to set your financial priorities straight. Learn to differentiate needs (what you need to survive) from wants (what you need to live comfortably).

Once you do, you’ll avoid borrowing unnecessarily, and it’ll become easy to stay away from loan traps.

6. Avoid Impulse Buying

Most people borrow from digital lenders because they cannot contain the excitement when seeing something nice. It could be trendy attire, a new phone model, or anything fashionable.

If you can avoid buying on impulse and first consider your priorities, you can avoid loan apps.

7. Create Another Income Stream

You can never make enough money in Kenya. There will always be more bills to pay, and that’s where the aspect of having multiple income streams come in.

Besides, they provide you with financial security in case one income stream shuts or fails to pick up.

8. Start Paying Off Your Debt

It’s vital to start paying off your outstanding debt as you avoid picking another.

One way to raise money for that is through asset liquidation. If you have something you can sell that won’t necessarily impact your way of living, sell it.

And if you already have multiple income streams, they can generate the money to pay down your debt.

9. Track Your Spending and Stay Accountable

You can only know if you are sticking to your budget if you can track your spending. It helps you to stay accountable for every financial decision you make.

Luckily, there are numerous tools you can use to track your spending, such as Spending Tracker, Money Lover, and Mint. These tools will help you track your expenses and budget for your finances.

10. Ask for Help from Financial Experts

We all need help at some point. Just like you need a doctor for your clinical issues, you need a finance expert on money matters.

As the Cent Warrior family, we can help you avoid the financial pitfall that loan apps create. We have developed a personal finance guide that you’ll find helpful in planning your finances and avoiding debt in general. Hopefully, it can be a start to your financial freedom.

Concluding Thoughts on Loan Apps in Kenya

It’s undeniable that loan apps are becoming a debt trap that most Kenyans, especially the youth, find hard to break free from. That, however, doesn’t mean that you have to give in to the pressure of borrowing.

As shared, you can prepare for financial emergencies by setting up a rainy day fund and living a modest life or finding ways to inject more cash flow.

If you need help to get started, talk to us on social media, and we’ll be happy to walk with you on this journey. We at Cent Warrior are about promoting a generation that’s financially and debt free, and it starts with breaking free from the loan app snare.

Also Read: