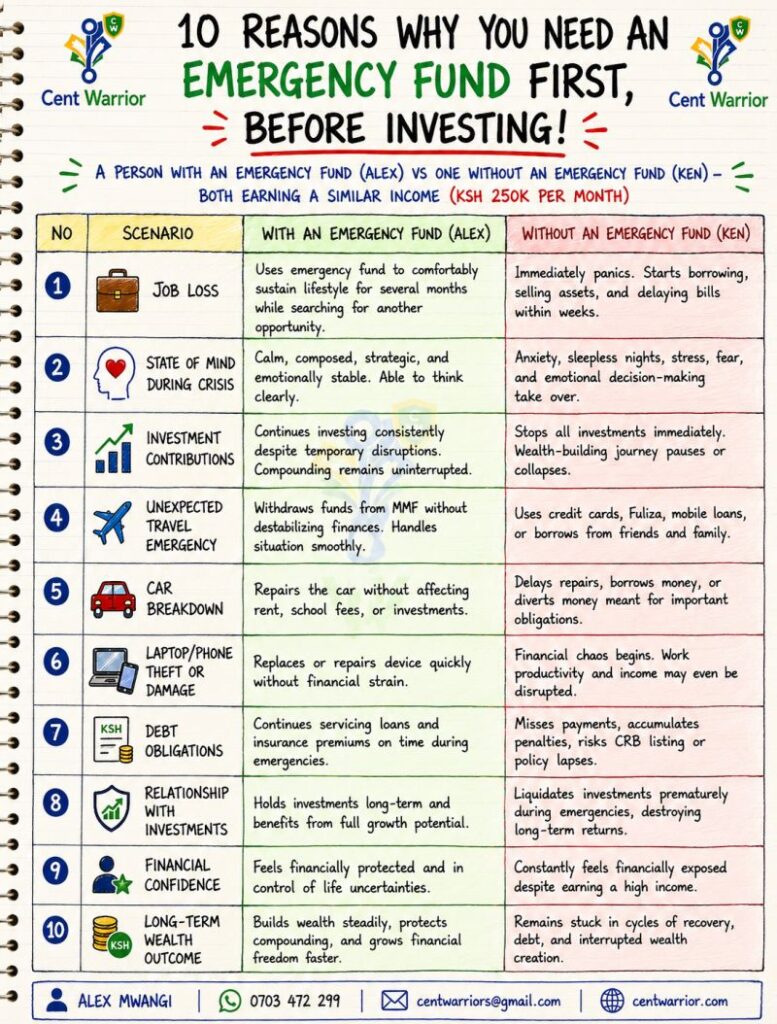

Most people calculate their emergency fund wrongly.

They only think about:

Rent

Food

Transport

And forget the financial obligations that do not stop when emergencies happen.

Listen carefully.

What Your Emergency Fund Should Really Cover

If you lose your job today…

Your Whole Life Insurance premiums will still be due.

Your debt repayments will still demand attention.

Your SACCO loan deductions will not pause.

Your children will still need support.

Your subscriptions, fuel, internet, and utilities will still exist.

Life does not become cheaper because you are going through a crisis.

This is why many people think they have an emergency fund…

Until the emergency actually comes.

Then panic begins.

The car breaks down unexpectedly.

Your laptop dies in the middle of work.

Your phone gets stolen.

An urgent family trip appears.

Income delays happen.

Retrenchment strikes unexpectedly.

And suddenly the emergency fund disappears in weeks.

Build a Realistic Survival Number

This is why your emergency fund must be intentional.

When calculating it, include:

Rent

Food

Transport

Insurance premiums

Debt repayments

Utilities

Family obligations

School support if necessary

Build a realistic survival number.

Not a fantasy number.

Because your emergency fund is supposed to protect your financial life during difficult seasons.

Not create another crisis halfway through the storm.

Aim for:

3–6 months minimum

12 months for stronger protection

And keep this money in an exclusive Money Market Fund.

Your emergency fund is not idle cash.

It is your financial oxygen tank.

If you need guidance on the best MMF for your emergency fund,

WhatsApp me “BEST MMF” on 0703472299.

Alex Mwangi | The Cent Warrior | WhatsApp 0703472299