You are here because one (or more) of these speaks to you:

- You want to invest for your child’s education but don’t know the optimal way to achieve it.

- You want to protect your children in case you’re no longer there to provide for them.

- You already bought an education policy but are unsure if it truly meets your needs.

- You now have new information and regret taking an education or endowment policy.

- You want to know the next step to cut your losses and catch up.

And here’s the good news—

You’re in the right place.

This group is where we go beyond the surface and tackle the deep, uncomfortable, but necessary truths about education planning and protection—topics very few are willing to talk about.

Here, we’ll:

- Break down the myths,

- Review real policies,

- Share experiences,

- And uncover practical solutions you can act on.

You will not only find clarity—you’ll find strategies that secure your children’s education without sabotaging your financial future.

Let’s begin with some of the burning questions already asked in this space…

The Truth About Education Policies

An education policy is a type of insurance and savings plan designed to help parents build a fund to pay for their child’s future education.

It combines investment and life insurance protection in one product.

Here’s how it works:

1️. Regular Contributions (Premiums)

You agree to pay a set amount of money monthly, quarterly, or annually for a fixed period (e.g., 10–18 years).

2. Savings/Investment Component

A portion of your premiums goes into an investment fund managed by the insurance company,

This grows over time to provide a lump sum or structured payouts when your child reaches school or university age.

3. Insurance/Protection Component

The other portion provides life cover.

If the parent (policyholder) dies or becomes permanently disabled during the policy term, the insurer either:

- Pays out the sum assured immediately, or

- Waives future premiums but still guarantees the child’s education fund at maturity.

4. Maturity Benefit

At the end of the policy term, you receive a lump sum or periodic payouts to cover school fees.

Why People Buy It

- Provides disciplined savings for education.

- Protects the child’s education even if the parent dies or can’t work.

- Sometimes includes extra benefits like critical illness cover.

Limitations You Should Know

- Returns are usually lower than market-driven investments (like Trust funds, Money Market Funds, fixed income funds or special funds).

- Policies can be rigid—cancelling early (before 3 years) may lead to loss of premiums.

- It’s more of a safety net + forced savings tool than a high-return investment.

In short:

An education policy is not the best pure investment or protection tool, but it is a protection + guaranteed savings plan for your child’s school fees.

Who Is an Education Policy Suitable For?

An education policy may be a good fit if you struggle with savings discipline. It works for someone who:

- Fears inconsistency – You’re worried you might not save consistently for the next 10–15 years for your child’s education.

- Fears early withdrawals – You know that if your savings are easily accessible, you might spend them before the goal time.

- Lacks better investment knowledge – You aren’t aware of other investment vehicles that balance both protection and growth.

- Doesn’t care about returns – Your priority is not maximizing profit, but simply having something guaranteed when your child gets to college.

But remember: an education policy often gives you the short end of the stick—limited protection and lower returns compared to other options.

In reality, your lack of discipline becomes the price you pay for this enforced savings.

Who Is an Education Policy NOT Ideal For?

Forget about an education policy if:

a) You’re financially disciplined and can consistently contribute to an education fund without touching it.

b) You prefer growth-focused investments such as:

- A Trust Fund (great for estate planning since it avoids probate)

- A Money Market Fund

- A Fixed Income Fund

- A Special Fund

- SACCO deposits for dividends

c) You already have whole life insurance in place to protect your income and secure your child’s future if you pass away.

Why Whole Life Insurance Matters

A whole life plan is designed to protect your income and give your loved ones financial security. It provides:

- A lump sum payout when you pass on—replacing your income so your family maintains their lifestyle (rent, mortgage, education, daily needs).

- Living Benefits that pay you a lump sum if you’re diagnosed with critical illnesses (Cancer, Heart Attack, Stroke, Coma, Paralysis, Open Heart Surgery) or suffer Accidental Disability.

My Winning Strategy

Instead of relying solely on an education policy, I recommend combining two pillars:

- A Pure Investment Education Fund – for maximum growth and returns.

- A Whole Life Insurance Policy – for maximum protection and guaranteed security.

That way, you’re not just saving—you’re protecting, investing, and building a future-proof plan for your children.

Are we together?

So, What Do You Do If You Already Have an Education Policy?

If you already secured an education policy and are now wondering what to do with it, here’s my advice:

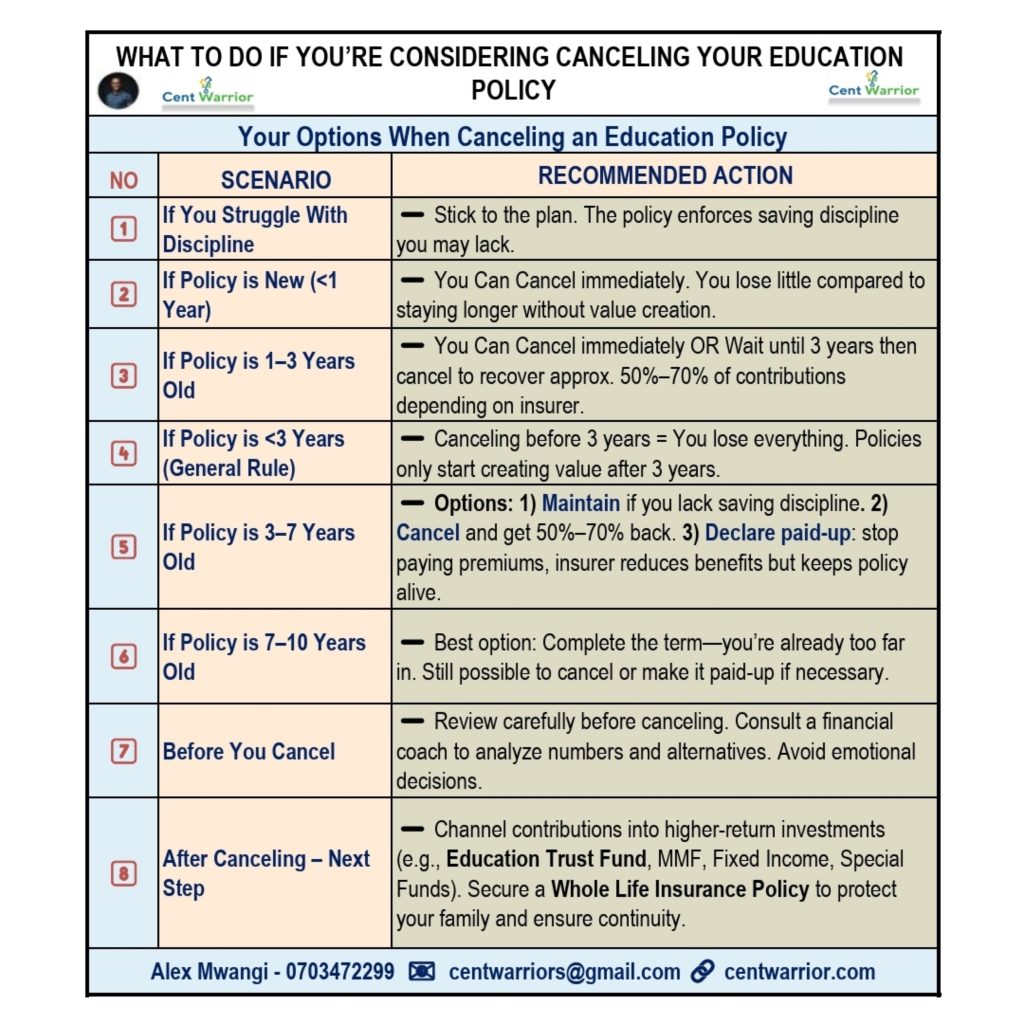

Example: 10-year Policy

If You Struggle With Discipline

If you know deep down that you lack the discipline to consistently save for your child’s education, stick to your plan.

The policy will enforce that discipline for you.

If Your Policy Is Still New (Below 3 Years)

You can Cancel.

- Canceling before 3 years = you lose everything.

These policies only start creating value after 3 years.

- If you’re between 1–3 years, you can OPT to wait until it hits 3 years.

At that point, you can cancel and recover about 50%–70% of your contributions (depending on the insurer).

- If you’re below 1 year, don’t even think about it—CANCEL immediately. It’s not worth it.

If Your Policy Is 3–7 Years Old

At this stage, you have three options:

- Maintain it if you lack the discipline to save elsewhere.

- Cancel it and receive 50%–70% of your contributions.

- Declare it paid-up—stop paying premiums, and the insurer will revise your benefits downward but keep the policy alive.

If Your Policy Is 7–10 Years Old

Honestly, just complete the term—you’re already too far in.

But if it pains you, you can still apply the above options (cancel, paid-up, or maintain).

Before You Cancel…

Don’t rush. These are real money decisions.

- Reach out to me and let’s review your policy numbers together.

- You can also share your policy here for quick feedback.

For a deeper, private review session, I offer this service at a small fee—to help you decide the smartest move with clarity and confidence.

Important Note

When you cancel, be ready to:

- Choose the best investment vehicle for higher returns.

- Secure a whole life insurance policy for maximum protection.

And I’m here to guide you on both fronts.