Forget the education policies and flashy education plans you’ve been hearing about for years.

I want you to pay attention.

What I am about to share will not only help you secure your child’s education, but also create your own financial freedom.

We are going to plant an Education Money Tree.

One that will serve your children and still take care of you in your old age.

The Education Money Tree Strategy

Here is the strategy:

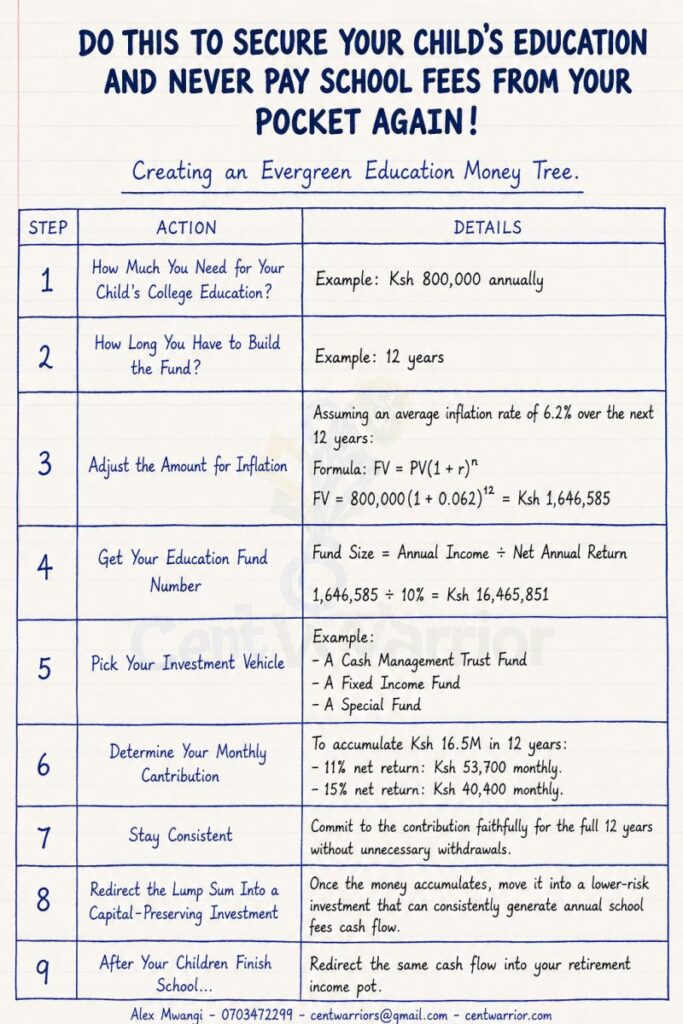

- Identify How Much You Need for Your Child’s College Education

Example: Ksh 800,000 annually

- Identify How Long You Have to Build the Fund

Example: 12 years

- Adjust the Amount for Inflation

Assuming an average inflation rate of 6.2% over the next 12 years:

Formula:

FV = PV(1 + r)ⁿ

FV = 800,000(1 + 0.062)¹²

= Ksh 1,646,585

Meaning:

Ksh 800,000 today will be equivalent to approximately Ksh 1,646,585 in 12 years.

This is the mistake many parents make.

They save using today’s numbers while education costs keep rising every year.

- Get Your Education Fund Number

Now ask yourself:

How much money must you accumulate in 12 years to generate Ksh 1,646,585 annually without exhausting the capital?

Formula:

Fund Size = Annual Income ÷ Net Annual Return

1,646,585 ÷ 10%

= Ksh 16,465,851

That means you need approximately Ksh 16.5 Million invested in a 10% average net return fund to sustainably generate your child’s annual school fees.

- Pick Your Investment Vehicle

Now it is time to invest.

Choose a vehicle capable of generating strong long-term growth.

This could be:

A Cash Management Trust Fund

A Fixed Income Fund

A Special Fund

- Determine Your Monthly Contribution

To accumulate Ksh 16.5M in 12 years:

At 11% net return compounded monthly:

You need approximately Ksh 53,700 monthly.

At 15% net return compounded quarterly:

You need approximately Ksh 40,400 monthly.

- Stay Consistent

Commit to the contribution faithfully for the full 12 years without unnecessary withdrawals.

Discipline is what turns this plan into freedom.

- Redirect the Lump Sum Into a Capital-Preserving Investment

Once the money accumulates, move it into a lower-risk investment that can consistently generate annual school fees cash flow.

- After Your Children Finish School…

Redirect the same cash flow into your retirement income pot.

Why This Structure Works

This is why I call it an Education Money Tree.

It keeps serving generations.

Now you may ask:

Alex, which structure would you personally recommend?

My favorite structure is:

A Cash Management Trust Fund + A Whole Life Insurance Policy

Why?

Because the Trust Fund protects your children’s education money from:

Creditors

Family conflicts

Probate delays

Financial scavengers

In case of your absence, your family accesses the money smoothly without waiting years for succession processes.

WhatsApp 0703472299