Before you rush there and hit the Bid button, we need to talk.

Everyone has an opinion about this IPO.

The debate is hot.

And the two camps arguing about KPC’s fair value are leaving many investors confused.

Let’s break it down clearly.

Camp 1: Transaction Advisors and Sponsors

They support the KSh 9.00 offer price and argue that:

- KPC has regulated and predictable cash flows

- It enjoys a dominant market share

- It operates like infrastructure with pricing power

- Long-term contracts and reserved pipelines support earnings

Their position: The company deserves a premium price.

Camp 2: Independent Research Houses

Several analysts disagree.

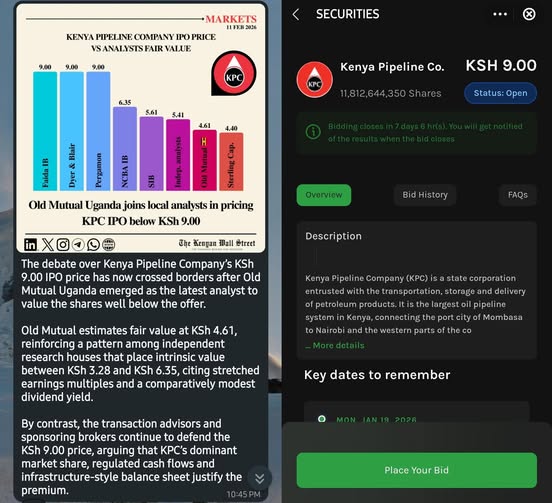

Here are their fair value estimates:

Faida IB — Ksh 9.00

Dyer and Blair — Ksh 9.00

Peregamon — Ksh 9.00

NCBA IB — Ksh 6.35

SIB — Ksh 5.61

Independent Analysts — Ksh 5.41

Old Mutual Uganda — Ksh 4.61

Sterling Capital — Ksh 4.40

Most independent valuations place intrinsic value between KSh 4.40 and KSh 6.35, well below the IPO price.

Their reasons?

Low dividend yield and stretched earnings multiples.

So Where Do You Stand? And What Does This Mean For You?

If you buy at Ksh 9.00:

- You may be paying above what many analysts believe the business is worth today.

- Long-term gains will depend heavily on earnings growth and dividend payouts.

If you care about value investing:

- Compare your expected return to the IPO price.

- Understand your risk appetite — infrastructure assets often take time to reward investors.

Now, does this eliminate your chances of benefiting from the IPO?

Absolutely not.

Here Is My Personal View (Not Investment Advice)

The market is full of buzz and emotion around this IPO.

And people will buy — whether the shares are overpriced or not.

At the entry point, fair valuation may not matter.

It will likely be overridden by emotion.

And in the short run, markets respond very well to emotion.

After listing, demand could push the price up — possibly above Ksh 10–15 as investors scramble to get a piece.

But then reality sets in.

Sanity creeps back.

Logic returns.

The market adjusts.

The price could fall below the IPO price of Ksh 9.00 and settle somewhere around Ksh 4.5–7.00, closer to intrinsic value.

After that, if the business delivers steady earnings, strong dividends, and growth, the price can rise again — but over years, not weeks.

Here Is What I Will Do

I will invest a small amount using Ziidi Trader to test my theory.

If the price spikes post-listing — say Ksh 12–15 — I may sell and lock in gains.

If I want to own KPC long term, I will wait for the market to adjust closer to intrinsic value and then buy heavily.

Simple. Strategic. Patient.

Now tell me:

Are you participating in this KPC IPO?

And what is your strategy?

Alex Mwangi

WhatsApp: 0703472299