Only 4% of Kenyans can afford a Ksh 10 million mortgage, according to a Business Daily report published on Tuesday, November 12, 2025.

That figure struck me deeply.

How many people truly earn an income that can sustain a mortgage worth over 10 million shillings?

And how does the monthly repayment look in reality?

The numbers are shocking.

Let’s do the math.

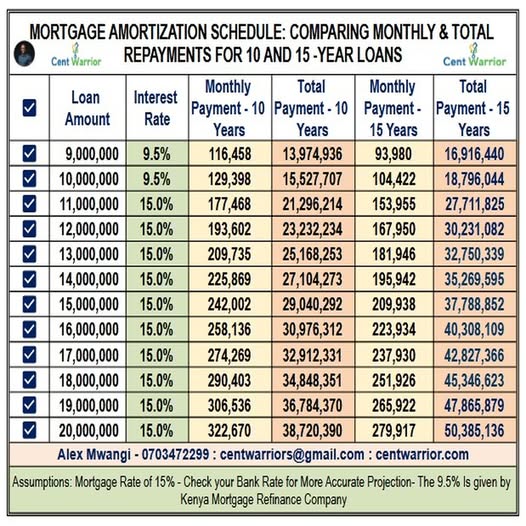

If you take a Ksh 15 million mortgage at an interest rate of 15%, with a 10-year period, you will be required to pay about Ksh 242,000 every month.

By the end of your repayment period, you will have paid Ksh 29,040,292 in total, almost double the original loan amount.

Now picture a young professional who just landed their dream job. They get excited, sign up for a 10- or 15-year mortgage, and feel proud to “own” a home.

But soon reality hits.

They are locked into heavy repayments for over a decade, barely able to save, invest, or pursue any other financial goals.

And with no job security in today’s economy, losing employment mid-way could be financially devastating.

Even worse, most end up sacrificing other key priorities such as emergency funds, insurance, education plans, and investments, just to keep up with the monthly mortgage.

So here’s the real question:

Is a mortgage truly the path to homeownership freedom, or a modern-day financial trap?

Would you rather take a mortgage, or buy land and build gradually?

Alex Mwangi | WhatsApp 0703472299

Here is a mortgage repayment schedule comparing 10-year and 15-year terms