It’s that mortgage conversation again!

Would you rather:

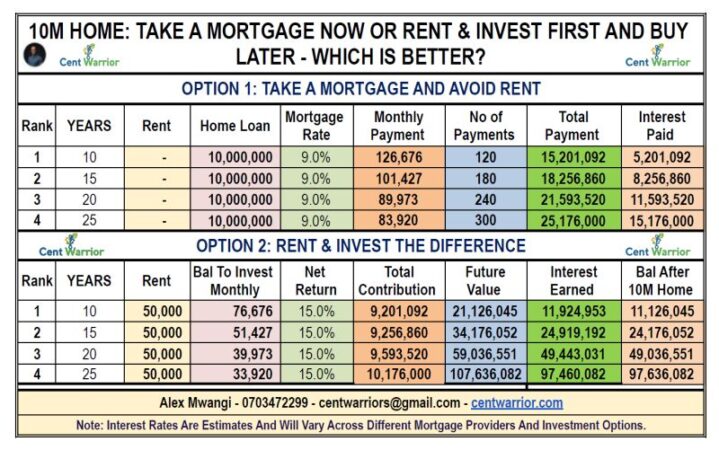

Take a Ksh 10M mortgage at 9% interest and stop paying rent?

OR

Continue renting a Ksh 50,000 apartment, invest the difference in a 15% net return fund, then buy your home later in cash?

Which option is more optimal?

Thanks to KMRC, single-digit mortgage rates averaging 9% are now becoming possible through partner banks.

This is a major shift considering we have been used to punitive mortgage rates of 13%–17%.

So let us look at the numbers.

Option 1 vs. Option 2

OPTION 1: Take The Mortgage

Buying a Ksh 10M home at 9% interest:

10 Years

Monthly: Ksh 126,676

Total Paid: Ksh 15.2M

Interest: Ksh 5.2M

15 Years

Monthly: Ksh 101,427

Total Paid: Ksh 18.3M

Interest: Ksh 8.3M

20 Years

Monthly: Ksh 89,973

Total Paid: Ksh 21.6M

Interest: Ksh 11.6M

25 Years

Monthly: Ksh 83,920

Total Paid: Ksh 25.2M

Interest: Ksh 15.2M

The longer the repayment period, the lower the monthly burden — but the more interest you pay.

By year 25, you will have paid more than double the original house value.

OPTION 2: Rent & Invest The Difference

Instead of taking the mortgage, continue renting at Ksh 50,000 and invest the difference into a 15% net return fund such as Mansa-X or Arvocap Almasi Fund.

Here is what happens:

Invest Ksh 76,676/month for 10 years = Ksh 21.1M

Invest Ksh 51,427/month for 15 years = Ksh 34.2M

Invest Ksh 39,973/month for 20 years = Ksh 59M

Invest Ksh 33,920/month for 25 years = Ksh 107.6M

Mind-blowing, right?

In 10 years, you could potentially afford two of those homes.

In 15 years, the equivalent of three homes.

The numbers clearly show that renting first and investing the difference appears to be the superior financial decision.

The Real Challenge: Discipline

But here is the uncomfortable truth:

Only about 10% of people can actually pull this off successfully.

Reason?

Human behavior.

The challenge is not knowledge. It is discipline.

Most people will invest consistently for a few months, then abandon the mission.

Others will divert the money midway.

That is why success with money is 80% behavior and only 20% head knowledge.

Sometimes the most logical financial strategy fails because emotions get involved.

So choose your hard wisely.

If you choose Option 1:

Pay off the mortgage aggressively and reduce interest exposure as quickly as possible.

If you choose Option 2:

Remain disciplined, seal all loopholes, and never interrupt the investment journey.

So, which option would be most ideal for you?

Alex Mwangi | The Cent Warrior | WhatsApp 0703472299