Not Fixed Income Funds.

Not Special Funds.

Not Equity Funds.

This might sound contrarian.

But hear me out.

I have seen too many people skip this step, only to end up with nothing solid to rely on in old age.

Some, out of financial ignorance, even withdraw their pension early—crippling their future retirement payout.

Now let’s get this clear.

Why is a pension contribution one of the most important investment decisions you will ever make?

A pension fund is not a flashy growth fund.

It won’t give you market adrenaline.

It won’t trend on performance charts.

It is that quiet, disciplined safety net growing steadily in the background.

You won’t see it shouting about winning returns.

But it is silently working for you.

- It protects you from your own indiscipline.

- No easy access.

- No emotional withdrawals.

- No impulsive decisions.

And in the background, compound interest is doing the heavy lifting.

Then one day—when your official years of productivity are over—it reappears.

Bold.

Confident.

Ready to sustain you.

And here is something powerful most people ignore:

The government protects you from yourself.

You are only allowed to access one-third of your lump sum.

The remaining two-thirds must purchase an annuity—guaranteeing you a monthly income for life.

That is structured dignity.

Here’s why I prioritize a pension before any other investment:

- It is low risk.

- It is heavily regulated by the Retirement Benefits Authority.

- The chances of losing your money are extremely remote.

In fact, pension funds under insurance companies are guaranteed funds.

There is a minimum declared return—often capped around 4%—below which the fund is not allowed to fall, regardless of market performance.

Tell me which equity or special fund gives you that kind of downside protection.

Before you chase high returns and higher risk, secure your foundation.

Start with your pension.

Allocate at least 10–15% of your income there.

Build your long-term dignity first.

As I emphasize in The 7-Step Wealth Masterplan (Get your copy in the comment section),

Wealth is not about excitement—it is about structure, protection, and sustainability.

Pension is structure.

Pension is protection.

Pension is sustainability.

Once that is in place, then you can build your Wealth Engine confidently.

If you have no idea which pension fund to choose,

WhatsApp me “PENSION” and I will guide you to the right one.

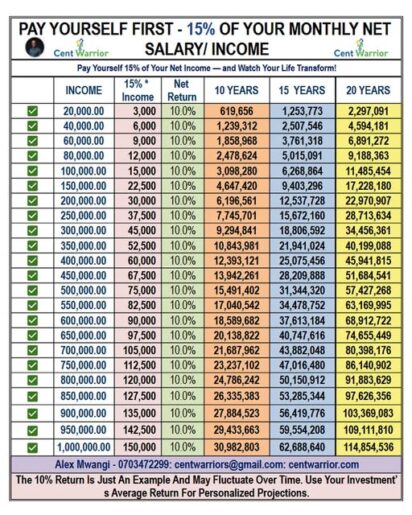

Now let me show you what happens when you consistently save 15% of your income in a pension fund earning 10% annually.

That’s where the real magic begins.

Alex Mwangi

WhatsApp: 0703472299