Is it that bad?

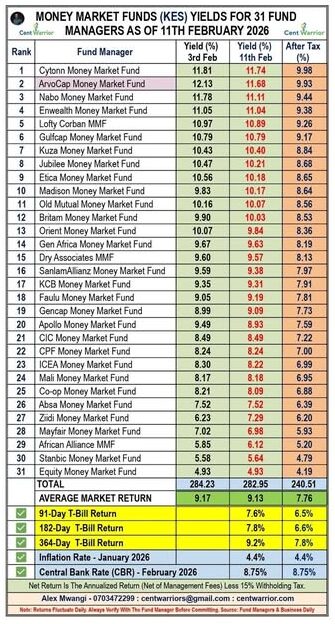

As at 11th February 2026, no MMF is giving a 10% net return.

The market is simply responding to declining interest rates.

The benchmark rate — the CBK rate — has dropped from 9% to 8.75%.

Naturally, yields across money market funds adjust downward.

At the same time, inflation stands at 4.4% (January 2026).

This means one thing:

Your money market fund must deliver a net return above 4.4% to preserve your purchasing power.

Anything below that?

You are technically losing ground.

Now let’s talk strategy.

If you are using a Money Market Fund for long-term wealth building, it’s time to rethink your positioning.

MMFs are not designed for aggressive growth.

They are designed for:

- Liquidity

- Stability

- Capital preservation

Nothing more.

If your goal is long-term growth, you should consider reallocating to:

- Fixed Income Funds like Arvocap Almasi Fixed Income Accumulation Fund

- Special Funds like Mansa-X

These vehicles have historically delivered 15%+ net returns over the long term, making them more suitable for wealth compounding.

Be strategic.

The only money that should comfortably sit in a Money Market Fund is:

- Emergency Fund

- Sinking Fund

That’s it.

Emergency money must remain accessible.

Sinking fund money must remain stable.

Growth money must grow.

If you are stuck in analysis paralysis wondering which MMF to open for your emergency or sinking fund, don’t overcomplicate it.

WhatsApp me “BEST MMF” and I will share my top 3 recommendations.

Otherwise,

Invest wisely.

Position correctly.

Let your money work with intention.

Alex Mwangi

WhatsApp: 0703472299