This will rattle some feathers.

But I’m ready to take the fire shots—

And defend my position with logic and numbers.

Come closer. Hear me out.

You might be holding an education policy that will shortchange you in the long run.

I’m almost certain you were sold the wrong product.

You have no idea how many people reach out to me—regretting their decision.

But by the time they do, it’s often too late to change course.

Let’s rewind.

Why did you buy that education plan?

Most of you were approached by an insurance agent who sold fear—not a solution.

She asked,

➖ “Mary (insert your name), what would happen to your children if you’re no longer here? Would they still go to college like you’ve envisioned?”

You paused…

You had no good answer.

And Agent Alex was ready to pounce with the ‘perfect’ solution—

An education policy that promised your family financial security in your absence or a mouthwatering lump sum after 10, 15, or 20 years of disciplined saving.

Afraid of missing out and exposing your children to risk, you signed the dotted line.

You didn’t pause to do the math.

You didn’t ask:

Is this the best way to protect my children?

Is this the optimal way to grow money for my child’s education?

You were sold a promise of “Ksh 3 million” at the end…

But what you bought was a slow, underperforming plan that grows your money at a snail’s pace.

Here’s what they didn’t tell you:

That plan is not an investment—it’s a basic savings and protection product.

Most education plans return between 2% and 6% annually.

Why?

Because your contribution is split between savings and insurance protection.

And guess what?

They never disclose how much goes where.

So you end up settling for the final payout—no clarity, no power to optimize.

In short:

Education plans are for people who struggle with savings discipline.

The price? Poor returns.

And yes, I’ll say it: It’s better to have something than nothing saved for your children.

But if you’re a DISCIPLINED SAVER, there’s a smarter way.

Here’s what you should do:

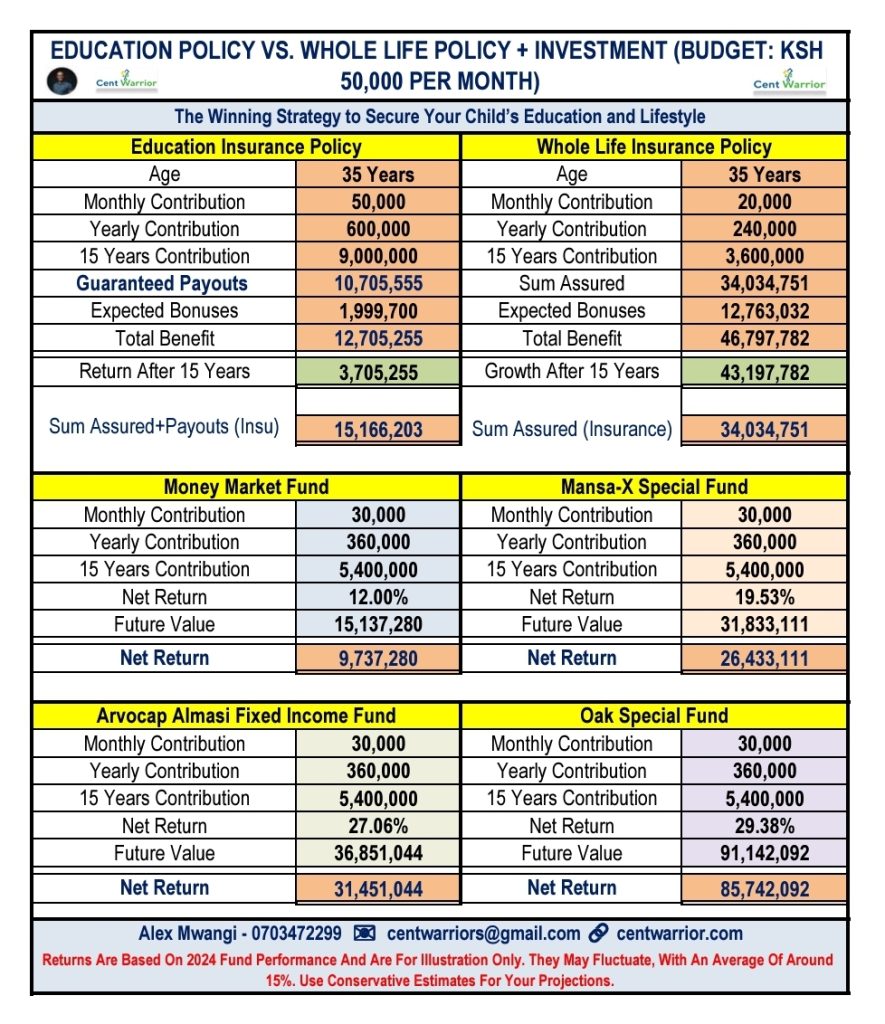

Step 1: Secure a Whole Life Insurance policy for the protection part.

This ensures your children are protected—whether you’re there or not.

Step 2: Open a high-growth fund—like a Money Market Fund, Fixed Income Fund, Special Fund, or a Trust Fund—to consistently invest for their education.

This combo gives you the best of both worlds:

Protection + Growth.

Imagine you have Ksh 50,000 per month.

Here’s a smarter distribution model:

Ksh 20,000 → Whole Life Insurance (protection)

Ksh 30,000 → Education Investment Fund (growth)

In 15 years, your child will have the funds they need

—And if something happens to you before then, the whole life cover takes care of it all.

Choose Strategy Over Emotion.

——–

Alex Mwangi | Your Personal Finance Architect

0703472299

Helping You Master Your Money | Build Wealth | Protect Your Legacy

Visit My Resource Hub Here: https://linktr.ee/centwarrior