This will ruffle some feathers again. But I’m ready for the heat — because numbers never lie.

Let’s talk facts.

Many parents proudly hold education policies thinking they’ve secured their child’s future. In reality, most of them are sitting on a financial trap that will shortchange them in the long run.

I’ve spoken to hundreds of parents — regret written all over their faces. By the time they discover the truth, it’s often too late.

Why Did You Buy That Education Plan?

Be honest.

Most of you didn’t go looking for it — someone sold it to you. You were approached by an insurance agent who played on your fears:

“Ann, what would happen to your children if you’re no longer here? Would they still go to school as you’ve planned?”

You paused… and fear did the rest.

They handed you a glossy brochure, painted a dream of guaranteed school fees, and a lump sum payout after 10, 15, or 20 years. And before you knew it, you signed.

But here’s the uncomfortable truth:

You didn’t buy a solution. You bought comfort for your fear.

You didn’t ask the real questions:

- Is this the best way to protect my children?

- Is this the best way to grow my money for their education?

If you did the math, you’d realize that you’re promised Ksh 3 million after 15 years — yet you’re paying in Ksh 2.7 million or more. The growth? Barely visible.

What They Never Told You

That “education policy” isn’t an investment.

It’s a savings-and-protection hybrid — one that grows at a snail’s pace, often between 2% and 6% per year.

Why so low? Because your premiums are split between savings and insurance cover. But they never show you how much goes where.

So, you end up with neither optimal protection nor meaningful growth. Just a polite thank-you letter and an underwhelming cheque.

Let’s Be Clear

- Education policies are for people who struggle with saving discipline and extremely risk-averse individuals.

- The price of convenience? Poor returns.

And while having something is better than nothing, there’s a smarter route — if you’re a disciplined saver.

Here’s What You Should Do Instead

Step 1: Separate Protection from Investment

Take a Whole Life Insurance Policy to handle the protection bit. That guarantees your children’s future — whether you’re here or not.

Step 2: Channel Growth into High-Return Vehicles

Invest monthly into a Money Market Fund, Fixed Income Fund, Special Fund, or Trust Fund. These grow faster, compound better, and give you liquidity.

This strategy gives you what most people never achieve:

Protection + Growth.

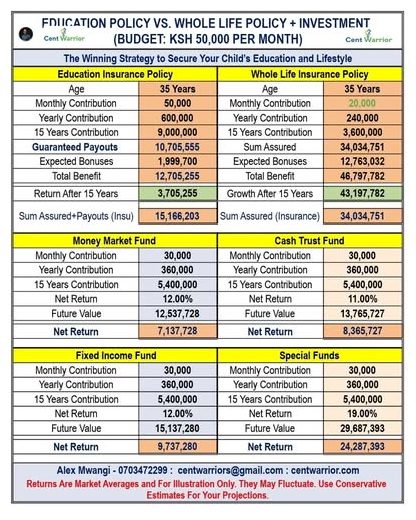

Let’s Put It in Numbers

If you can set aside Ksh 50,000 per month, do this:

- Ksh 20,000 → Whole Life Insurance (Protection)

- Ksh 30,000 → Education Investment Fund (Growth)

In 15 years, your child will have the education fund ready.

And if life happens before then — the Whole Life cover ensures your dream lives on.

That’s strategy over emotion.

If you’re still confused about all this, just WhatsApp me — I’ll help you structure the best winning strategy for your child.

Alex Mwangi | WhatsApp → 0703472299