Popularized by Massachusetts senator and 2020 Democratic Party presidential candidate Elizabeth Warren in her 2005 ‘All Your Worth’ financial book, the 50/30/20 budget rule is one of the most popular and easy-to-follow budgeting formulas today.

All it takes is to split your after-tax into 50% needs (necessities), 30% wants (comforts and fun), and 20% money goals (such as savings, debt down payments, and investment).

While it’s called a budgeting rule, the 50/30/20 rule is ideally a percentage-based guide that anyone, especially those new to budgeting, can follow.

But does that make it realistic for everyone? Of course not, and as I’ll explain later, one of its criticisms is that the percentages don’t change with income or financial goals change.

This guide shall help you understand the 50/30/20 rule better to decide whether to use it. Here’s what to look forward to:

- What is the 50-30-20 budgeting rule?

- What are the 50/30/20 budget’s pros and cons?

- Who uses the 50/30/20 budget rule?

- How do you budget with the 50/30/20 rule?

- 50/30/20 rule example

- Is the 50/30/20 rule realistic?

- 50/30/20 Rule vs. Zero-Based Budgeting

- Is 50/30/20 Budgeting good for you?

Let’s dive into it!

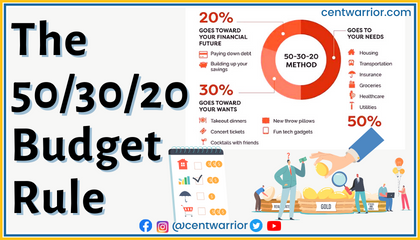

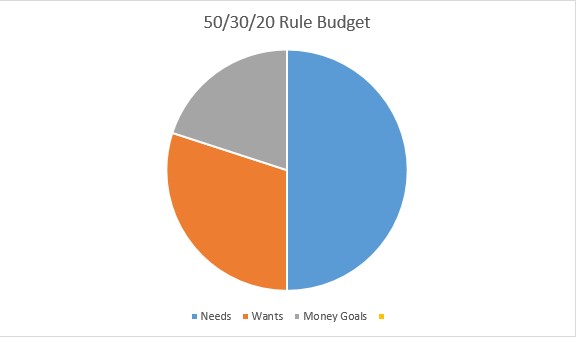

What’s The 50/30/20 Budget Rule?

The 50/30/20 Rule is a percentage-centered budgeting guide that focuses on splitting your after-tax into these three categories:

- Needs (50%)

- Wants (30%)

- Money goals (20%)

This budgeting guide, initially known as the 50/20/30 Rule, was popularized by the current Massachusetts Senator Elizabeth Warren in her famous 2005 financial book All Your Worth.

50% Needs

There are the essential things you must live with and, therefore, must pay for. Needs should take 50% of your after-tax income, and they include the following:

- Food and groceries

- Housing (rent or mortgage)

- Utilities (gas, electricity, and water)

- Minimum debt payments

- Healthcare costs

- Insurance costs

- Transport costs

- School fees

30% Wants

The wants are the non-essentials that add fun and comfort to your life. They are the things that make you enjoy life, and according to the budgeting rule, they should take up not more than 30% of your after-tax.

These expenses include:

- Dine-outs

- Subscriptions

- Entertainment

- New clothes

- Vacations

- Trips

- Hobbies

- New gadgets

- Spa

- Personal care

20% Money Goals

Money goals differ between people, but some of the most important ones, which should only take 20% according to this rule, are:

- Building an emergency fund

- Paying down debt

- Saving for retirement

- Starting a sinking fund (for college fees, house deposits, business startups, or any other large purchase).

Since you only allocate 20% of your after-tax to your money goals, some may be unattainable since the allocation is too small. This is another criticism of the 50/30/20 Rule. It tends to focus more on basic needs, and fun/wants – not money goals.

Pros and Cons of The 50-30-20 Rule of Budgeting

The Pros of 50/30/20 Budgeting

Ideally, the 50/30/20 Rule comes with these advantages:

- Simplicity – The 50/30/20 budgeting only features three major categories requiring you to split your income. So, there isn’t much calculation, and it’s easy to understand, making it suitable for those who wish to learn how to budget money.

- Inclusivity – While the percentage allocation for the three categories differs, the budgeting guide doesn’t leave any category out. It includes them all (needs, wants, and money goals) and allows you to adjust.

- Minimal tracking – While every budgeting requires tracking for accountability reasons, you don’t have to do much of it with a 50/30/20 budgeting rule. That’s another reason it’s suitable for those new to budgeting.

- Ideal for decent income earners – If you earn a decent income (not very small or very high), the 50/30/20 Rule works just fine. You just need to know your expenses and allocate your money to the three categories correctly.

The Cons of 50/30/20 Budgeting

Although 50/30/20 budgeting has some advantages, it equally has some concerns, which include the following:

- Less attention on money goals – Realistically, what can you do regarding saving and investments with only 20% of your income? Remember, the 20% also caters to paying down your loan and any sinking fund you might have. In my view, the allocation is too small.

- Relatively static – A good budget should change with your money goals and income. The 50/30/20 budgeting is quite the opposite. All three percentages remain the way they are when your money goals and income changes, making it hard to attain your new goals.

- Does not work for every income range – While the 50/30/20 budgeting is ideal for a decent income, it doesn’t suit people or a meager income and those with a very high income. For those on a meager income, the 50% needs allocation may be too small for the necessities, while for those on a huge paycheck, the 20% money goals allocation may not match their financial goals.

- Unattainable in high-cost areas – Regardless of income size, you may have difficulty adjusting to the 50/30/20 rule if you live in a high-cost area. As long as the cost of living is high, you may need to change your budget allocation, which the 50/30/20 does not allow you to do.

Who’s 50/30/20 Budgeting for?

The 50/30/20 rule is not for everyone who wants to budget. It’s specifically designed for these categories of people:

- Those on a decent income

- Those very new to budgeting

- People who aren’t good with budget tracking and want a simple way to do it

- Those who may want to save but still cater to their basic needs and have some fun

Conversely, the 50/30/20 rule doesn’t suit those on a meager income or very high salary scale. That’s because the first category may have more needs which may need more than 50% of their salary, while the second category may have more money goals for which the 20% budget allocation may not be enough.

How to Do The 50-20-30 Budget Rule

Here are six steps to creating a 50/30/20 budget:

Step 1 – Determine Your After-Tax Income

If you are on a payroll, you wouldn’t have to do any calculations here, as what you get is after-tax. But if you’re a freelance or contract worker, you may need to work out your after-tax based on how much you make monthly.

Just deduct the tax amount after talking to a tax professional.

Step 2 – Track Expenses from The Previous Month

To quickly determine your expenses, track how you spent the previous month and list all the costs. Remember to categorize them as needs and wants, and don’t forget the money goals.

Step 3 – Limit Needs (Necessities) to Only 50% Of Your Take-Home Pay

Go ahead and budget to spend 50% of your take-home pay on the necessities. If the needs cost more than 50%, you must reduce some of them.

Step 4 – Limit Wants (Fun) To 30% Of Your Take-Home Pay

Also, adjust your wants to ensure you don’t spend more than 30% of your after-tax. Overall, these are easier to adjust to than basic needs because you can live without them.

Step 5 – Allocate the Remaining 20% To Money Goals

Once you limit needs and wants to 50% and 30%, respectively, put the remaining 20% on your money goals. It could be more if you manage to cut down on some wants.

Step 6 – Start Budgeting and Stick to It

Now that you know how you should spend your money, go ahead and do it. The goal is not to make a budget but to use it. So, track out to ensure you live by it and stay accountable.

50/30/20 Budget Example

Let’s take an example of an entry-level manager of job Group D1 who takes home an average of Ksh 80,000 per month.

Here’s the breakdown

- Needs (50% of Ksh 80,000 = Ksh 40,000)

- Wants (30% of Ksh 80,000 = Ksh 24,000)

- Money goals (20% of Ksh 80,000 = Ksh 16,000)

You can break such an allocation as follows:

| Needs Food/groceries – Ksh 10,000 Rent – Ksh 12,000 Utilities (electricity, gas, and water) – Ksh 5,000 Healthcare – Ksh 5,000 Insurance – Ksh 3,000 Transport – Ksh 3,000 Miscellaneous – Ksh 2,000 Sub-Total – Ksh 40,000 | Wants Dine-outs – Ksh 4,000 Subscriptions – Ksh 4,000 Trip – Ksh 5,000 Personal care (Nail and Hair) – Ksh 3,000 Others – Ksh 8,000 Sub-Total – Ksh 24,000 Money Goals Emergency fund – Ksh 10,000 Other savings – Ksh 6,000 Sub-Total – Ksh 16,000 |

Is The 50/30/20 Rule Realistic?

Not everyone will find the 50/30/20 Rule realistic. One article by Yahoo shows that 50/30/20 budgeting is very restrictive and fails to consider your lifestyle, financial goals, and values.

You cannot save more than 20% with a 50/30/20 Rule, and the budget allocation does not change when your income and money goals change.

And concerning lifestyle changes, someone on a low income may need more than 50% to meet basic needs. So, the rule is less adaptive to income and lifestyle changes.

Moreover, the budget may be unrealistic for people in high-cost areas, especially those in a low-to-average income bracket, since they’ll need more than 50% to pay for inevitabilities like housing, food, and healthcare.

That, however, doesn’t mean that 50/30/20 Budgeting will never work. For example, it’s realistic when one earns a decent income and has fewer money goals. It also works for someone who’s never budgeted before and wants to give it a go.

50/30/20 Rule Vs. Zero-Based Budgeting

Let me first define zero-based budgeting before comparing it with 50/30/20 Budgeting. In zero-based budgeting, the difference between your income and expenses is zero. The reason is that you give a job for every cent you make.

Now into the comparison;

A zero-based budget offers flexibility, something you don’t get from a 50/30/20 budget. For example, we’ve seen that the percentage allocation in a 50/30/20 budget doesn’t change even if you’ve more needs than wants or more money goals than needs.

The situation is, however, different in a zero-based budget. A zero-based budget is adjustable depending on your financial needs and money goals bracket, unlike the 50/30/20 Budget Rule.

But for the best results, especially when trying to get out of debt, combine zero-based budgeting with Dave Ramsey’s famous seven baby steps:

The baby steps are as follows:

- Save $1000 (or Ksh 100,000) first in a starter fund if you make a similar amount or more or twice your monthly expenses if you make less than Ksh 100k

- Pay off all your debt (apart from the mortgage) using the snowball method

- Complete the funding of your emergency fund to equal 3 – 6 months of your living expenses

- Put 15% of your income in a retirement plan

- Set up a children’s school fund

- Pay off your house

- Build wealth and remember to give a part of it to charity

Is The 50/30/20 Budgeting Rule Good for You? Closing Remarks

There’s no doubt that the 50/30/20 budget rule is simple to work out and understand, and that’s why it’s ideal for those new to budgeting. It’s also perfect for those on a decent income.

However, the budgeting rule may not be ideal if your money goals, income, or lifestyle change. Moreover, budgeting can be too restrictive in a meager income, very high-income bracket, or even a high-cost area.

In such cases, we recommend zero-based budgeting, which our Cent Warrior team on social media can help you understand more if you need clarification.

Also Read: