Let me show you how one financial decision can cost you a jaw-dropping Ksh 317 Million.

Yes — that’s how much you could potentially lose by taking the mortgage route blindly.

Before emotions take over — and I get it, owning a home feels good.

In fact, securing a home for your family is one of the best decisions you can ever make.

But let’s dare to examine the logic behind the numbers.

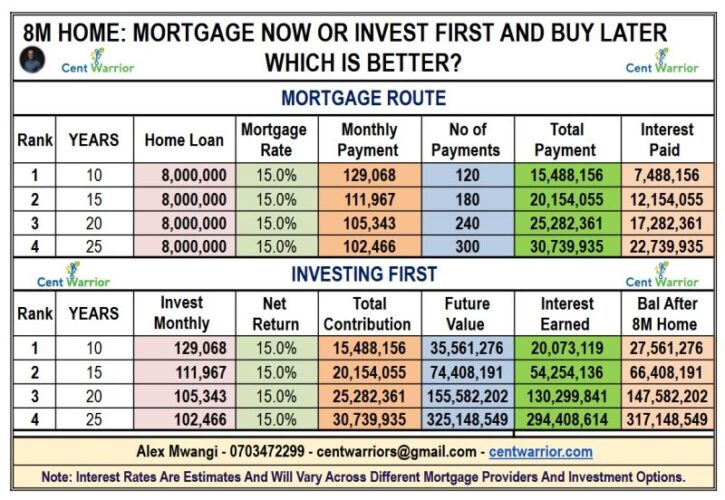

Should You Buy an 8M Home Now Using a Mortgage…

OR

Delay gratification, invest first, then buy later?

Scenario 1: Buy Now Using a Mortgage

Buying an 8M home at 15% interest:

10 Years = Ksh 15,488,156 (Monthly Payment: Ksh 129,068)

15 Years = Ksh 20,154,055 (Monthly Payment: Ksh 111,967)

20 Years = Ksh 25,282,361 (Monthly Payment: Ksh 105,343)

25 Years = Ksh 30,739,935 (Monthly Payment: Ksh 102,466)

Let that sink in.

A 15-year mortgage will cost you over Ksh 12.15M in interest alone.

A 25-year mortgage?

You will pay over Ksh 22.7M in interest.

That is almost 3 extra homes gone.

Scenario 2: Delay Gratification & Invest First

What if you invested those same monthly amounts into a 15% net return investment instead?

Here’s what happens:

Invest Ksh 129,068/month for 10 years = Ksh 35.6M

Invest Ksh 111,967/month for 15 years = Ksh 74.8M

Invest Ksh 105,343/month for 20 years = Ksh 155.6M

Invest Ksh 102,466/month for 25 years = Ksh 325.1M

Read that again carefully.

With just 10 years of disciplined investing at Ksh 129,068/month, you could buy your 8M home in cash…

and still remain with Ksh 27.6M.

The Real Cost of Financial Choices

Here is the uncomfortable truth.

The mortgage route gives you instant gratification.

But the investor mindset gives you:

The home

The investment portfolio

The passive income potential

The financial freedom

That is how wealthy people think.

But let me also be honest:

This route only works if you have:

Extreme discipline

Patience

Emotional control

Long-term thinking

A solid investment plan

And truthfully?

Most people struggle with delayed gratification.

That’s why many end up trapped in long-term debt cycles.

But the math does not lie.

Now tell me:

Would you rather…

Own a home quickly but spend 2–3x more?

OR

Wait, invest wisely, and eventually own both the home and your financial freedom?

Important Assumptions

This analysis is based on average mortgage rates of 15% across banks and estimated 15% net annual investment returns. It does not include stamp duty, legal fees, valuation fees, insurance, maintenance costs, or other related charges.

Alex Mwangi | The Cent Warrior | WhatsApp 0703472299